One sentence. 8 models. The whole experiment.

Every model received the identical one-line brief and ran the same 11-role pipeline — discovery, two sprints, security, a performance pass, reviewed PRs, to a live app. 7 of 8 shipped green; cost ran from $0.52 to $73.00 AUD — a 143× spread, and price didn't predict quality. Below: every app (thin-pipeline and native-agent build), full telemetry, and a code/design/review quality read.

The apps it built

Same brief, 8 designs. Click any to open it live. Badge = does it actually compute when you use it.

✓ works

✓ works ✓ works

✓ works ✓ works

✓ works ✓ works

✓ works ✓ works

✓ works ✗ broken

✗ broken ✗ broken

✗ broken ✗ DNF

✗ DNF…and the same models in their native agent

The thick-harness builds — each model's own coding agent (Claude Code / MiMoCode), run at max. Click to open live. DeepSeek & GLM were broken in the thin pipeline — they work here.

✓ works

✓ works ✓ works

✓ works ✓ works

✓ works ✓ works

✓ works ✓ works

✓ worksThin harness vs thick — the same model, built two ways

Each model's app from my thin API pipeline vs its own native agent (Claude Code / MiMoCode, at max). Click a badge to open that app live.

| Model | Thin · API pipeline | Thick · native agent |

|---|---|---|

| GLM-5.1 | broken | works ↳ fixed |

| Kimi K2.6 | DNF | works ↳ fixed |

| DeepSeek V4-Pro | broken | works ↳ fixed |

| MiniMax M3 | works | works |

| MiMo (Max Mode) | works | works |

By the numbers

Config (how each was tuned) · cost + output tokens · and the quality scorecard from the run. *All costs in AUD (USD list prices × 1.42, Jun 2026). GLM is free on the Z.AI plan; $/M shown is list price. tok/s = output ÷ total wall-time (effective throughput, includes self-heal rounds).

| Model | Thinking | Max out | $/M in·out | Cost | Out tok | tok/s* | Heals | Bugs/false | Security | Perf | App |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Fable 5Anthropic | Adaptive (always-on) | 128K | $14.20/$71.00 | $73.00 | 260K | 117 | 1 | 1/4 | clean | 4.9x | works |

| GPT-5.5OpenAI | Reasoning: xhigh | 128K | $7.10/$42.60 | $40.24 | 859K | 108 | 4 | 3/2 | hardened | 105.9x | works |

| Gemini 3.1 ProGoogle | Reasoning: high | 64K | $2.84/$17.04 | $0.93 | 33K | 18 | 3 | 5/0 | hardened | 1.4x | works |

| GLM-5.1Z.AI · free on plan | Thinking: on | 128K | $1.99/$6.25 | $2.12 | 302K | 78 | 5 | 3/2 | clean | 127.3x | broken |

| DeepSeek V4-ProDeepSeek | Think-Max | 384K | $0.62/$1.24 | $5.50 | 1012K | 54 | 11 | 4/1 | clean | 61.5x | broken |

| Kimi K2.6Moonshot | Thinking: 64K budget | 256K | $1.35/$5.68 | $2.52 | ✗ DNF — thrashed in the thin pipeline (201m at PR-1, never converged); ships clean in its native agent (24/24) | DNF | |||||

| MiMo v2.5 ProXiaomi | Reasoning: high | 128K | $0.62/$1.24 | $0.52 | 340K | 211 | 2 | — | 1.6x | works | |

| MiniMax M3MiniMax | Adaptive | 512K | $0.43/$1.70 | $1.52 | 626K | 237 | 3 | — | 73.6x | works | |

Does the premium model actually code better?

Beyond price and speed — code, design and review quality, read straight from the artifacts (every model's engine, architecture doc and PR reviews). Short answer: a little — and not in proportion to price.

Rankings, read from the artifacts — every model's output graded on five axes by reading the actual code, designs, reviews, tests and requirements. No model wins more than two, and rank doesn't track price.

| Dimension | Best → | middle | → Worst | ||

|---|---|---|---|---|---|

| Code (the engine) | Fable | GPT | Gemini 93¢ | MiniMax · GLM · Kimi · MiMo | DeepSeek $5.50 |

| Design & architecture | Fable | GPT | GLM | MiMo · Gemini · DeepSeek | MiniMax |

| Review judgement | Gemini 93¢ | DeepSeek | GPT | GLM · MiMo | Fable $73 |

| Tests (QA + security) | GPT $40 | Fable | MiniMax | DeepSeek · MiMo · Gemini | GLM · Kimi |

| Requirements (BA) | Fable | MiniMax | Gemini · MiMo | DeepSeek · GLM | GPT $40 |

The sharpest finding: GPT ($40) wrote the best tests but the worst requirements — worker-thread timeout isolation + exact-dollar anchors, yet vaguer acceptance criteria than a 52¢ model. Money buys test rigour, not requirements clarity. And MiMo (52¢) never ranked last on any of the five axes.

Which model for which job — route by stakes

The rankings as a procurement rule: default to cheap; pay up only where a wrong answer is genuinely expensive. The same call a bank makes on any control — match the spend to the risk.

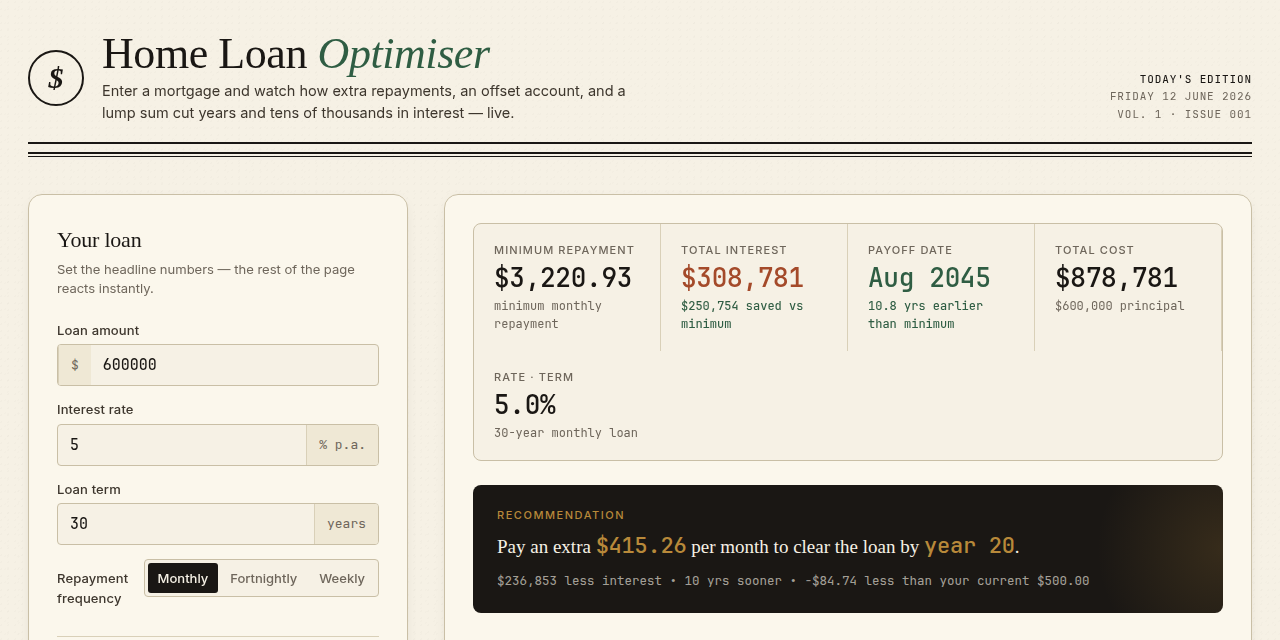

Real correctness bugs the cross-check surfaced — all 8 nailed the core maths ($3,220.93/mo); these are edge cases:

Eight personalities

Same brief, same harness — but each model has a character. What's distinctive about each.

By role — what the AI did for your job

Every role in the room, done by 8 models. Pick yours and see how each approached it.

The Architect designs the API & system.

You are the SOFTWARE ARCHITECT for a pure client-side static web app (no backend; all financial logic in one tested JS module loan.mjs — pure functions; a thin HTML/JS UI with sliders + an SVG chart). The engine must handle amortisation, extra repayments, an offset account, a lump sum, scenario comparison, a quote(loan, strategy) summary, and a recommendStrategy() that finds the smallest extra repayment hitting a target payoff. In ≤18 lines: the approach, the module API (export names + what each does), the data-model fields, a small ASCII box diagram (≤72 chars), the 2 key trade-offs and the single biggest technical risk. «BA requirements» «brief»

▸ OUTPUT · what each model produced:

**ARCHITECTURE — Home Loan Optimiser (≤18 lines)**

1. **Approach:** Every feature is one period-by-period simulation fold in `loan.mjs` — interest accrues each period on `max(balance − offset, 0)`, rounded to the cent; extra/offset/lump are just strategy inputs to that single loop. UI is a dumb shell: any input change re-calls the engine and redraws (no maths in UI).

2. **API (ESM, object args):**

3. `repayment(loan)` → per-period annuity payment (FR2 golden anchor, e.g. $2,997.75).

4. `simulate(loan, strategy)` → `{rows[], totalInterest, totalMonths, payoffDate}` — handles all features combined.

5. `quote(loan, strategy)` → `{repayment, totalInterest, totalMonths}` (thin wrapper over simulate).

6. `compare(loan, strategies[])` → per-strategy quote + `interestSaved`/`monthsSaved` vs baseline (drives FR7 cards).

7. `recommendStrategy(loan, targetMonths)` → linear scan of candidate extras (coarse $25 steps, refine $1) for the smallest hitting target — payoff is monotone in extra, so the scan is trivially correct; bisection is a later optimisation if ever needed.

8. **Model (plain JSON):** loan `{principal, annualRate, termYears, frequency}` · strategy `{extra=0, offset=0, offsetGrowth=0, lump:{amount, month}|null}`

9. row `{period, interest, principal, balance}` · all money rounded to cents at exactly one place (interest accrual) to prevent drift.

```

+----------------------+ quote/compare/ +----------------------+

| index.html + ui.js | recommendStrategy | loan.mjs (pure ESM) |

| sliders, SVG chart, |------------------->| simulate() core fold |

| cards — zero maths |<-------------------| quote/compare/rec |

+----------------------+ plain JS objects +----------------------+

```

**Trade-off 1:** Simulation over closed-form formulas — closed form can't express offset+lump+extra combined; ~360 iterations is far inside the 50 ms NFR, so we buy exactness for negligible perf cost.

**Trade-off 2:** Recompute-everything on input over incremental/memoised updates — stateless engine keeps UI trivially correct under FR6's <100 ms budget; we waste cycles but eliminate cache-invalidation bugs.

**Biggest risk:** Per-period rate convention for weekly/fortnightly (annualRate/52 vs /26 vs compounding-equivalent) plus the rounding policy — the one thing likely to break to-the-cent golden tests (FR2/FR3). Lock it with reference fixtures *before* any UI work.Approach: Static app: `loan.mjs` is the only finance engine (pure/tested); responsive WCAG UI maps forms/sliders to data, renders cards/SVG, and fires one analytics event after first valid compare.

Amortise period-by-period using canonical frequencies/dates; offset interest base is `max(balance-offset,0)`, and dated events apply at the first period date `>=` selected date.

API exports: `validateLoan(input)` -> canonical loan or errors.

`repaymentFor(loan)` -> scheduled repayment when amount omitted/term-driven.

`amortise(loan,strategy={})` -> rows applying recurring extras, offsets/changes, lump sums.

`quote(loan,strategy)` -> `{repayment,totalInterest,totalMonths}` summary.

`compareScenarios(loan,namedStrategies)` -> baseline vs each `{totalInterest,interestSaved,timeSaved,payoffDate}`.

`chartSeries(schedule)` -> `{balance[],cumInterest[],payoff[]}` for SVG.

`recommendStrategy(loan,targetMonths,candidates)` -> linear scan extra amounts, return smallest meeting target.

Loan model: `{balance,annualRate,termYears,repaymentFreq,repaymentAmount?,startDate}`.

Strategy model: `{extras:[{amount,freq,start,end}],offset:{balance,changes:[{date,balance}]},lumps:[{amount,date}]}`.

Result rows: `{date,opening,interest,scheduled,extra,lump,offset,principal,closing,cumInterest}`; result adds `payoffDate`.

`+-------------+ +------------------+ +--------------+`

`| HTML UI |--->| loan.mjs pure |--->| Cards + SVG |`

`| WCAG forms |<---| tests/fixtures | | analytics |`

`+-------------+ +------------------+ +--------------+`

Trade-offs: full recompute vs caching (simpler/testable, still <1s for 40y weekly x3); fixed amortisation rules vs bank-specific quirks (explainable but not every lender).

Biggest risk: ambiguous date/payment/interest ordering causing $/period mismatches—freeze rules in fixtures and surface assumptions in UI.**Approach:** A reactive architecture where vanilla JS UI listeners feed state to pure functions in `loan.mjs`, driving instant DOM and raw SVG updates to guarantee <200ms latency.

**Module API (`loan.mjs`):**

- `amortize(loan, strategy)`: Computes `[{month, balance, interest}]` array.

- `quote(loan, strategy)`: Returns aggregated `{repayment, totalInterest, totalMonths}`.

- `compare(base, opt)`: Returns delta `{interestSaved, monthsReduced}`.

- `recommendStrategy(loan, targetMonths)`: Binary searches smallest extra repayment.

**Data Models:**

- `Loan`: `{ principal, annualRate, termMonths }`

- `Strategy`: `{ extraRepayment, offsetBalance, lumpSum, lumpSumMonth }`

- `Result`: `{ repayment, totalInterest, totalMonths, schedule }`

**Architecture Diagram:**

`[Vanilla JS/HTML UI] --(Loan & Strategy)--> [loan.mjs Pure Math Engine]`

`[Raw SVG Chart & DOM] <---(Result Models)---| `

**Key Design Trade-offs:**

1. *Native SVG generation vs. Chart libraries:* Prioritizes zero-dependency bundle size and instant render performance (NFR1) over development convenience.

2. *Binary search vs. Algebraic formulas:* Iterative search in `recommendStrategy` handles offset/lump-sum edge cases cleanly, trading minor compute cycles for logic simplicity.

**Biggest Technical Risk:**

JavaScript IEEE 754 floating-point inaccuracies compounding over 360 monthly iterations; necessitates strict rounding to cents at every amortization step to ensure financial accuracy.**Approach:** Unidirectional UI binds slider inputs directly to pure functions in `loan.mjs`, instantly mapping returned state to an SVG path renderer to ensure frictionless, live-updating charts.

**Data Model:** `Loan`={balance, rate, termMonths}; `Strategy`={extraRepay, lumpSum, offset}; `Result`={repayment, totalInterest, totalMonths, schedule[]}.

**Module API (`loan.mjs`):**

* `quote(loan, strategy)`: Core engine computing the amortization schedule and returning the `Result` summary.

* `recommendStrategy(loan, targetMonths)`: Scans candidate extra repayments to find the smallest one hitting the target payoff.

* `compare(baseResult, optResult)`: Generates scenario comparison returning `{interestSaved, monthsSaved}`.

**Architecture:**

`+--[ UI (Sliders/HTML) ]--+ +--[ loan.mjs ]--+ +--[ SVG Chart ]--+`

`| input.oninput -> state | -> | quote(l, s) | -> | render(schedule)|`

`+-------------------------+ +----------------+ +-----------------+`

**Trade-offs:**

1. Recalculating the entire schedule on every slider tick (simpler pure stateless UI) over implementing complex partial-caching (better CPU usage).

2. Strict monthly compounding over complex exact-daily accrual (guarantees NFR1 <200ms response time, slightly sacrificing day-level precision).

**Biggest Technical Risk:** Cumulative floating-point precision errors in JS compounding over a 360-month schedule, causing penny-level drift from strict banking standards (AC2).Approach: Pure client-side app with `loan.mjs` pure functions; UI sliders + SVG chart; localStorage scenarios.

API: quote(loan,strat)->{repayment,totalInterest,months}; recommendStrategy(loan,target)->{extra,quote}; generateSchedule(loan,strat); compare(q1,q2); isValidLoan(l).

Models: Loan{principal,rate,term,freq}; Strategy{extra,offset,lumps[]}; Quote{repay,totalInt,months,sched}.

Diagram:

+-------------+ +-------------+

| UI |<--->| loan.mjs |

+-------------+ +-------------+

| localStorage (scenarios) |

+---------------------------------+

Trade-offs: 1) cent-integer rounding vs BigDecimal for <500ms chart updates and ±$0.01 precision. 2) constant offset & one lump sum vs full txn history to keep engine simple and testable.

Risk: floating-point drift causing non‑zero terminal balance; forced zero & cent‑integer arithmetic eliminate it.## `loan.mjs` — Architecture (≤18 lines)

**Approach:** Model the loan as a month-by-month balance array; each pure function applies one strategy modifier per iteration, yielding an immutable `Result` object. A thin UI wires sliders to recompute on `input` and repaints an SVG path via `requestAnimationFrame`.

**API:**

```js

// Core

amortise(loan) → Result // baseline schedule

applyExtra(loan, extra) → Result // +regular extra $/m

applyOffset(loan, balance) → Result // interest on (bal - offset)

applyLump(loan, month, amount) → Result// one-off at month N

combine(loan, ...modifiers) → Result // compose multiple strategies

// Utilities

quote(loan, strategy) → { repayment, totalInterest, totalMonths }

compare(baseline, optimized) → { interestSaved, monthsSaved, percentSaved }

recommendStrategy(loan, target) → Strategy // binary-scan smallest extra hitting targetMonth

// UI helpers (thin layer, not in engine)

renderChart(resultA, resultB) → SVGElement

bindInputs(formEl) → ReactiveLoan

```

**Data model:**

```ts

Loan = { principal, annualRate, termMonths }

Result = { schedule: {month, payment, interest, principal, balance}[],

totalInterest, totalMonths, repayment }

Strategy = { extra?: number, offset?: number, lump?: {month,amount} }

```

**Box diagram (≤72 chars):**

```

┌──────────────────────────────────────────────┐

│ HTML/JS UI (sliders, chart, compare view) │

│ bindInputs() ──► reactive Loan object │

├──────────────────────────────────────────────┤

│ loan.mjs (pure functions, zero DOM) │

│ quote() compare() recommendStrategy() │

│ amortise │ applyExtra │ applyOffset │ lump │

├──────────────────────────────────────────────┤

│ Storage: none — recomputed each interaction │

└──────────────────────────────────────────────┘

```

**2 Key trade-offs:**

1. **Full schedule array vs. running totals** — storing every month costs memory (up to 360 rows) but makes chart rendering O(1), comparison trivial, and debugging by inspection; recomputing totals-only would save bytes but break AC4.1's clickable data points.

2. **Binary-scan recommendStrategy vs. closed-form** — scanning extra-payment values with `quote()` is O(log N × term) which stays under 1s for any realistic range; an algebraic solver would be faster but wrong once offset/lump modifiers introduce non-linearity into the balance curve.

```

APPROACH Pure daily-interest engine in one ES module (loan.mjs); thin HTML/SVG UI debounces input and encodes full state in URL hash, with localStorage for named scenarios.

API (loan.mjs, all pure)

amortise(loan, strategy) -> schedule[] // month rows

quote(loan, strategy) -> {repayment,totalInterest,totalMonths} // summary for tiles/URL

recommendStrategy(loan, target) -> {extraMonthly,lumpSum,monthsSaved} // $1-step linear scan: smallest extra hitting targetMonths (simplest correct, exploits monotonicity)

compareScenarios(loan, strats[]) -> quote[] // drives 2-3 side-by-side tiles

applyOffset(principal, offset) -> effectivePrincipal // test seam

DATA

loan : {principal, ratePct, termYears, freq:'W'|'F'|'M', startDate}

strategy : {extraMonthly=0, offsetBalance=0, lumpSum=0, lumpMonth=0} // 0 = feature off

row : {month,date,opening,interest,repayment,principal,closing}

result : {repayment,totalInterest,totalMonths} // quote() shape

DIAGRAM

[UI+URL#s=] -50ms-> [loan.mjs] -schedule/quote-> [SVG x3 + tiles]

^ |

+------------ localStorage scenarios <---------------+

TRADE-OFFS T1 Daily correctness vs cost: precompute a day-indexed effective-principal array (P - offset - extras-so-far), then aggregate into months — keeps amortise() O(months) yet cent-exact.

T2 URL-shareable state vs payload bloat: JSON in #s= base64 + CompressionStream at save time — zero-backend portability in exchange for a one-time encode cost.

RISK Off-by-one-cent drift in daily offset/lump-sum application breaks the "matches CBA/ANZ/NAB/Westpac to the cent" AC. Mitigation: golden-test fixtures against published tables plus property tests (closing balance strictly non-increasing; Σrow.interest == result.totalInterest).

```The PO frames the vision & success metric.

You are the PRODUCT OWNER. In ≤4 lines total: (1) a one-sentence product vision and the primary user; (2) ONE measurable success metric; (3) the top 3 priorities (what matters most). Product: «the one-line brief»

▸ OUTPUT · what each model produced:

1) **Vision:** A live, interactive Home Loan Optimiser that shows everyday borrowers — primary user: an Australian homeowner with a variable-rate mortgage — exactly how extra repayments, an offset account, or a lump sum cut total interest and years off their loan, with charts that update as they type. 2) **Success metric:** ≥80% of first-time users reach an "insight moment" (view a strategy comparison showing interest saved + time cut) within 60 seconds of entering their loan details. 3) **Priorities:** (a) Correct amortisation maths — results must match bank calculators to the cent; (b) Instant what-if interactivity — sliders/inputs re-render charts live with zero page reloads; (c) Clear side-by-side strategy comparison (baseline vs extra repayments vs offset vs lump sum) showing $ interest saved and payoff date.

Vision: Help mortgage holders optimise repayments by instantly comparing extra repayments, offset accounts and lump sums to save interest and repay sooner. Success metric: ≥60% of users complete at least one scenario comparison in their first session. Top 3 priorities: accurate loan calculations; simple scenario inputs; clear live charts showing interest saved and payoff date.

**Vision:** To empower everyday homeowners to achieve financial freedom faster by instantly visualizing how strategic payments slash their loan lifespan and interest. **Success Metric:** Achieve a 45% completion rate of users entering their baseline loan details and actively manipulating the live scenario charts. **Top 3 Priorities:** 1) Flawless, instantaneous financial calculation engine; 2) Engaging, real-time interactive data visualization; 3) Frictionless UX that makes entering complex financial details effortless.

1) **Vision & User:** Empower existing homeowners to rapidly eliminate mortgage debt by visualizing the real-time financial impact of extra repayments, lump sums, and offsets. 2) **Success Metric:** The percentage of users who input their baseline mortgage data and generate at least one customized, interactive savings projection. 3) **Top 3 Priorities:** 1) An accurate, lightning-fast calculation engine; 2) highly responsive, intuitive live charts; 3) a frictionless, simple UI for data entry.

Empower homeowners to cut mortgage interest and time via live simulations of extra repayments, offset accounts, and lump sums. Success metric: monthly active users completing at least one full what-if scenario. Top priorities: 1) calculation accuracy & trust, 2) real-time chart interactivity, 3) flexible what-if modelling.

**Vision:** Empower homeowners to reduce debt faster by simulating repayment strategies, targeting mortgage holders. **Success Metric:** Monthly interactions (simulations run & charts viewed). **Top 3 Priorities:** 1. Core repayment scenarios (extra payments, offset, lump sum). 2. Live, intuitive charts showing interest saved and time reduction. 3. Mobile-friendly interface for quick calculations.

**1) Vision & User:** Empower Australian homeowners and first-home buyers to make their mortgage disappear faster by instantly modelling how extra repayments, offset accounts, and lump sums reshape their loan — all through live, interactive charts. **2) Success Metric:** 40% of visitors who enter a loan scenario share, save, or return to compare ≥2 strategies within 7 days (proves real decision-making value, not just curiosity clicks). **3) Top Priorities:** • **Accurate math engine first** — 3 repayment strategies (extra, offset, lump sum) with month-by-month recalculation matching major bank formulas; trust dies instantly if the numbers are wrong. • **Live, responsive charts** — interest saved, time shaved off the loan, and balance curve all update in <200ms as the user types; this is the "aha" moment and the product's reason to exist. • **Scenario comparison view** — side-by-side comparison of 2–3 strategies so users can confidently choose the best path before talking to their lender. *Deferred: bank API sync, export-to-PDF, mobile native app — all nice, none are the wedge.*

The BA writes the requirements & acceptance criteria.

You are the BUSINESS ANALYST. The PO has defined the product vision «PO output». Write structured requirements in ≤12 lines: (1) functional requirements — what the system must DO; (2) testable, measurable acceptance criteria for each; (3) non-functional requirements. Product: «brief»

▸ OUTPUT · what each model produced:

**REQUIREMENTS — Home Loan Optimiser (BA, v1)** 1. **FR1 Loan input:** Capture principal, annual rate, term (years), repayment frequency (weekly/fortnightly/monthly). *AC:* invalid/out-of-range values show inline errors; charts never render NaN. 2. **FR2 Amortisation engine:** Compute repayment, per-period interest/principal split, total interest, payoff date. *AC:* matches reference values to the cent (e.g. $500,000 @ 6.00% p.a., 30yr monthly → $2,997.75/mo) via golden tests for ≥5 known scenarios. 3. **FR3 Extra repayments:** User sets recurring extra amount. *AC:* schedule recalcs; interest saved ($) and time cut (yrs+months) shown, exact to the cent vs baseline. 4. **FR4 Offset account:** User sets offset balance (and optional monthly growth). *AC:* interest accrues on (principal − offset) each period, never negative; savings reported vs baseline. 5. **FR5 Lump sum:** User sets amount + month applied. *AC:* balance drops at that month; remaining schedule recalcs; payoff date moves correctly. 6. **FR6 Live interactivity:** Sliders/inputs re-render all charts and figures on change. *AC:* update <100 ms, zero page reloads, no flicker. 7. **FR7 Strategy comparison:** Side-by-side view of baseline vs FR3/FR4/FR5 (combinable). *AC:* each card shows $ interest saved + new payoff date; reachable within 2 interactions of entering loan details (supports 60-sec insight metric). 8. **NFR:** Single-page client-side app, no backend or external calls; all maths in one pure engine module (UI must call it, never reimplement); recompute full 30yr schedule <50 ms; works offline in modern browsers; WCAG AA contrast. Handing to ARCHITECT: the pure-engine/UI split in NFR is the load-bearing constraint — design around it.

1. **FR1 Loan setup:** User can enter loan balance, interest rate, term, repayment frequency/amount and start date; **AC:** valid inputs generate a baseline showing repayment amount, total interest and payoff date. 2. **FR2 Extra repayment scenario:** User can add recurring extra repayments with amount, frequency and start/end dates; **AC:** system shows interest saved and payoff-date reduction versus baseline. 3. **FR3 Offset account scenario:** User can enter offset balance and optional balance changes; **AC:** interest is calculated on loan balance minus offset balance, never below zero. 4. **FR4 Lump sum scenario:** User can add a one-off repayment amount and date; **AC:** system applies it on the selected date and recalculates interest saved and payoff date. 5. **FR5 Scenario comparison:** User can compare baseline against extra repayment, offset and lump sum scenarios; **AC:** comparison displays total interest, interest saved, time saved and final payoff date for each. 6. **FR6 Live charts:** System displays charts for loan balance, cumulative interest and payoff timeline; **AC:** charts update automatically after input changes within 1 second. 7. **FR7 Completion tracking:** System records when a user completes at least one valid scenario comparison; **AC:** analytics can report first-session comparison completion rate. 8. **NFR Accuracy:** Calculations must match defined amortisation rules within $1 and 1 repayment period for standard test cases. 9. **NFR Usability:** Scenario inputs must be simple enough to complete a comparison in under 2 minutes for first-time users. 10. **NFR Performance:** Results and charts must update in ≤1 second for loans up to 40 years with at least 3 scenarios. 11. **NFR Accessibility/Responsive:** Interface must work on mobile and desktop and meet WCAG 2.1 AA for key form and chart interactions.

**Functional Requirements & Acceptance Criteria:** **FR1 Baseline Entry:** The system must capture initial mortgage details (principal, interest rate, term) via a frictionless UI. *AC1: Users can complete baseline data entry in ≤3 steps, with inputs auto-formatting as currency/percentages instantly.* **FR2 Scenario Modeler:** The system must allow users to apply extra regular repayments, offset account balances, and lump sums. *AC2: Adjusting any scenario slider or input field successfully calculates the new loan lifespan and total interest.* **FR3 Live Visualization:** The system must render interactive charts comparing the baseline loan trajectory versus the optimized scenario. *AC3: Charts dynamically update to explicitly display "Total Interest Saved ($)" and "Years Reduced" upon any variable change.* **Non-Functional Requirements:** **NFR1 Performance:** The financial calculation engine and chart rendering must execute updates in <200ms to feel instantaneous (Priority 1). **NFR2 Usability:** The interface must be mobile-responsive and require zero page reloads to minimize friction (Priority 3). **NFR3 Analytics:** The system must track "baseline complete" and "chart manipulated" events to measure the 45% completion success metric.

**1) Functional Requirements:** * FR1: System must capture baseline mortgage data (balance, rate, term) and optimization variables (extra repayments, lump sums, offset balance). * FR2: System shall calculate and output a comparison of baseline vs. optimized amortization schedules (total interest saved, time eliminated). * FR3: System must generate interactive, live-updating charts visualizing the principal vs. interest breakdown and loan term reduction. **2) Acceptance Criteria:** * AC1 (Data Entry): Users can input all baseline data and generate an initial customized projection in ≤ 3 primary actions/clicks. * AC2 (Accuracy): Calculated outputs must match standard financial amortization math exactly (to the dollar and day). * AC3 (Live Charts): Visual charts must automatically reflect any input adjustments without requiring a manual "refresh" button. **3) Non-Functional Requirements:** * NFR1 (Performance): The calculation engine must process and render projection updates in under 200 milliseconds. * NFR2 (Usability): The data entry interface must be frictionless, using intuitive sliders/fields that allow completion in under 60 seconds.

Functional Requirements: 1) Loan input: principal, rate, term, frequency. 2) Extra repayment: monthly extra. 3) Offset account: balance. 4) Lump sum: amount & date. 5) Live amortisation chart. 6) Scenario manager: save, name, compare. Acceptance Criteria: 1) Input: valid 1k-10M, 0.1-30%, 1-40yr; inline errors & defaults. 2) Extra: interest saved ±$0.01; chart updates <1s. 3) Offset: net balance interest; savings ±$1; chart reflects offset. 4) Lump sum: principal reduces on date; recalc matches manual. 5) Chart: <500ms update on change; hover tooltip. 6) Scenarios: persist across sessions; side-by-side delta view. Non-Functional: Performance: chart <500ms, load <3s. Accuracy: cent‑level vs standard amortisation. Reliability: 99.9% uptime. Usability: >80% first‑session scenario completion.

**Home Loan Optimiser – Structured Requirements** **Functional Requirements (FR):** 1. **FR1:** Input mortgage details (principal, rate, term). 2. **FR2:** Simulate extra regular payments, offset account balance, and lump sum scenarios. 3. **FR3:** Calculate and display original vs. optimized total interest, time saved, and total savings. 4. **FR4:** Generate live, interactive charts (e.g., amortization curve, interest comparison). 5. **FR5:** Interface must be responsive for mobile devices. **Acceptance Criteria (AC):** 1. **AC1.1:** System accepts principal ($100k–$2M), rate (1–15%), and term (1–30 years). 2. **AC2.1:** Extra payment input alters repayment schedule correctly; savings increase. 3. **AC2.2:** Offset balance reduces calculated interest; chart updates instantly. 4. **AC3.1:** Output shows >0% interest reduction for any valid extra payment scenario. 5. **AC4.1:** Charts reflect current inputs without page reload; data points are clickable/tappable. 6. **AC5.1:** Layout adapts without horizontal scroll on screens <768px wide. **Non-Functional Requirements (NFR):** 1. **NFR1:** Calculation engine returns results within 1 second. 2. **NFR2:** WCAG 2.1 AA compliant for core inputs/outputs. 3. **NFR3:** Data remains local to the device; no external storage required.

**Requirements — Home Loan Optimiser** 1. **Loan Input Capture** — Principal ($), interest rate (% p.a.), remaining term, repayment frequency (W/F/M), start date. *AC: Validates positive numerics within realistic ranges (rate 0–25%, term 1–40yr); state URL-encoded so any scenario is shareable.* 2. **Strategy Configuration** — User enables/configures independently: (a) extra recurring repayment, (b) offset account balance, (c) one-off lump sum at month N. *AC: Baseline (no strategy) always rendered; savings view requires ≥1 strategy enabled; all values editable after run.* 3. **Amortisation Engine** — Daily-interest, reducing-balance calc; offset reduces effective principal each day; lump sum applied at chosen month; extras reduce principal immediately. *AC: Output matches published CBA/ANZ/NAB/Westpac amortisation tables to the cent on reference cases; full month-by-month schedule generated.* 4. **Live Recalculation** — Full schedule recompute + chart redraw on every input keystroke. *AC: p95 latency <200ms on mid-range laptop; calc runs off main thread for terms >30yr; no input lag, no jank.* 5. **Visualisations** — Three live charts: (i) balance curve (baseline vs strategy overlay), (ii) cumulative interest saved, (iii) time shaved off loan. *AC: Re-render synchronously with input; ARIA labels + keyboard-accessible tooltips; colour-blind safe palette; show exact $ and months.* 6. **Scenario Compare** — Save named scenarios; load 2–3 side-by-side in comparison view. *AC: Each tile displays interest paid, total term, monthly repayment, interest saved, time saved; persisted in localStorage; deletable.* 7. **Share / Save / Return** — Copy shareable URL, email snapshot, or save to local library; returning visitors see prior scenarios. *AC: Share event fires analytics; URL round-trips full state; 7-day re-engagement supported to satisfy success metric.* 8. **NFR – Performance:** First contentful paint <2s on 4G; JS bundle <300KB gz; charts via SVG/Canvas. 9. **NFR – Trust:** In-app "How we calculate" panel discloses formula, rate assumptions, RBA source; no hidden rounding. 10. **NFR – Privacy:** Loan data stays client-side until user explicitly saves/shares; no third-party trackers pre-consent. 11. **NFR – Compatibility:** Latest 2 versions of Chrome, Safari, Edge, Firefox; responsive 360px–1920px. 12. **NFR – Accessibility:** WCAG

The UX sets the visual direction.

You are the UX/UI DESIGNER for a Home Loan Optimiser. In ≤10 lines define the visual direction: a named style, the colour palette (hex), a type pairing, the layout (hero figure, control panel, balance chart), and the 3 signature components. Dark, modern, high-contrast fintech with confident hierarchy. Product: «brief»

▸ OUTPUT · what each model produced:

**Style: "Midnight Ledger"** — dark luxury fintech, editorial hierarchy, glassmorphic depth on a near-black canvas.

**Palette:** `#0A0E1A` canvas, `#131A2E` raised surfaces, `#F4F6FB` primary text, `#8B93A7` muted; accent `#3DDC97` (savings/gain), `#5B8CFF` (baseline/interactive), `#FF6B6B` (interest/cost). Colour is semantic only — green is always money saved.

**Type:** Space Grotesk (display/numerals, tabular figures for dollar amounts) + Inter (UI/body).

**Layout:** Full-bleed hero figure — the headline *is* the number ("$184,302 saved · 6.4 yrs sooner") at `clamp(3rem,7vw,8rem)`, live-updating. Below, asymmetric split: left third is a sticky control panel (loan inputs, extra-repayment slider, offset toggle, lump-sum field), right two-thirds the balance chart — baseline vs optimised curves with shaded interest-saved delta, crossover annotated.

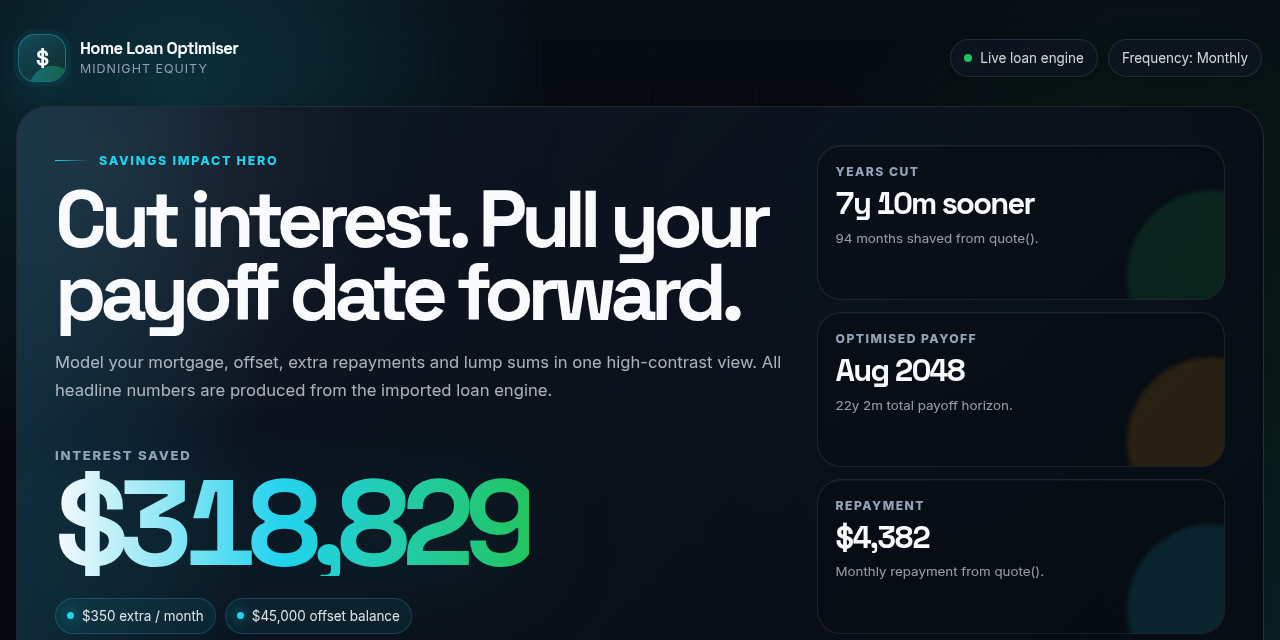

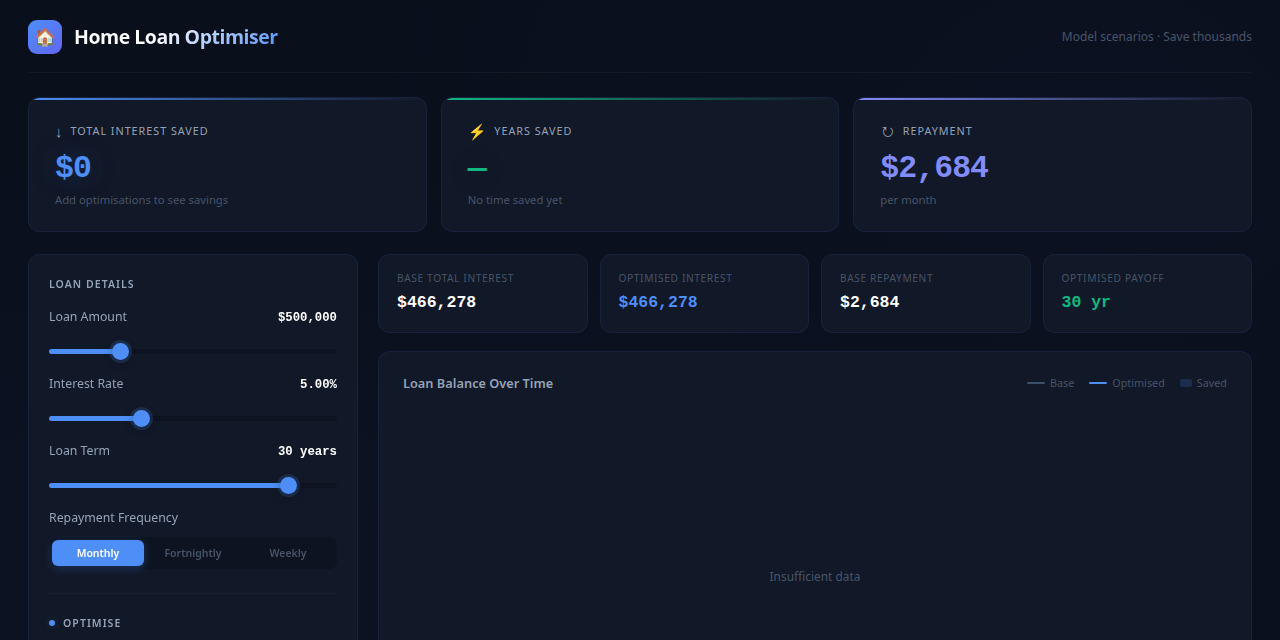

**Signature components:** (1) **Delta Hero** — the giant animated savings counter that reflows on every input; (2) **Strategy Cards** — stacked glass toggles (Extra / Offset / Lump-sum), each wearing its own live mini-stat; (3) **Payoff Timeline** — horizontal year-rail with draggable lump-sum marker and a "loan-free" flag that slides left as you optimise.1. **Style:** “Midnight Equity” — dark, modern, high-contrast fintech with confident hierarchy and crisp data storytelling. 2. **Palette:** Ink #070B12, Charcoal #111827, Electric Cyan #22D3EE, Profit Green #22C55E, Alert Amber #F59E0B, Soft Slate #94A3B8, White #F8FAFC. 3. **Type pairing:** Space Grotesk for bold figures/headlines + Inter for controls, labels, and explanatory text. 4. **Layout:** Top hero figure showing “Interest saved / Years cut” → left control panel for mortgage, offset, extra repayments, lump sum → right live balance chart. 5. **Signature component 1:** Scenario Toggle Cards — Base Loan, Extra Repayments, Offset Account, Lump Sum. 6. **Signature component 2:** Savings Impact Hero — oversized animated dollar saving, payoff date, and time shaved off. 7. **Signature component 3:** Dual-Line Balance Chart — original loan vs optimised loan with payoff milestone markers.

**Style:** "Luminous Fintech Noir" — a dark, high-contrast aesthetic with a confident, data-driven hierarchy.

**Palette:** Deep Void (#0B0D14), Surface (#151A24), Primary Text (#FFFFFF), Profit Green (#00E599), and Offset Purple (#8B5CF6).

**Typography:** *Space Grotesk* (bold, geometric hero numbers) paired with *Inter* (crisp, highly legible UI and chart data).

**Layout:** An asymmetrical split-screen interface maximizing real estate for live, reactive financial modeling.

**Control Panel:** A sticky left-hand sidebar housing sleek inputs, toggles, and sliders for seamless scenario testing.

**Hero Figure:** Top right, a massive, glowing metric ("Total Interest Saved") instantly anchoring the user's ultimate goal.

**Balance Chart:** Directly beneath the hero, a prominent, dynamic chart comparing the base loan against the optimized timeline.

**Signature Component 1:** Haptic-style dark sliders with vivid #00E599 neon track fills for dialing in extra monthly repayments.

**Signature Component 2:** A dual-layered, gradient Area Chart with glowing trajectory lines that animate instantly upon any input change.

**Signature Component 3:** Luminous "Milestone Tags" — interactive floating tooltips on the chart pinpointing exactly when the loan is cleared.**Style:** "Midnight Ledger" — a dark, high-contrast fintech aesthetic emphasizing confident hierarchy and financial clarity. **Palette:** Base `#0B0F19` (Void), Surface `#161B26`, Text `#F8FAFC` (White), Accent `#00F0A0` (Neon Mint), Alert `#FF4757` (Debt). **Typography:** *Space Grotesk* (headings/hero data) paired with *Inter* (body/UI) for a highly legible, modern geometric look. **Layout:** A responsive 2-column dashboard: a left "Control Panel" input sidebar, and a right Main View housing the "Hero Figure" and "Balance Chart". **Hero Figure:** A massive, dynamically calculating "Total Interest Saved" metric pinned at the top right, glowing neon mint upon value changes. **Control Panel:** A sleek, dark-matte card with segmented toggles (Extra Repayments, Offset, Lump Sum) and responsive, futuristic sliders. **Balance Chart:** An interactive, gradient-filled area chart contrasting the slow original amortization curve with the fast optimized burn-down schedule. **Component 1:** "Glowing Slider Knobs" — custom sliders with haptic-feel UI that emit a subtle neon mint shadow as users drag them. **Component 2:** "Timeline Milestones" — interactive pin-drops on the chart's X-axis highlighting the exact month/year the loan is paid off. **Component 3:** "Savings Summary Pill" — a floating, sticky bottom bar displaying live net savings, updated loan term, and CTA to "Lock in Strategy".

Visual direction: **Midnight Ledger** — dark, high-contrast fintech with a sharp numerical focus. **Colour palette:** `#0B0E14` (bg), `#151A24` (surface), `#00E5A1` (primary/mint), `#FF5C5C` (alert), `#FFD166` (highlight), `#F1F5F9` / `#8B9DC4` (text). **Type pairing:** *Space Grotesk* (headings) + *Inter* (UI) + *Fira Code* (data/tables). **Layout:** Split dashboard — left control panel (sliders, inputs); right hero figure (3D house with dynamic “savings halo”) above a live balance comparison chart. **3 signature components:** 1. **Scenario Slider Stack** — tactile extra repayment, offset & lump-sum sliders with real‑time calculations. 2. **Dual Balance River Chart** — animated filled area showing original vs. optimised balance over time. 3. **Break-Even Countdown Card** — radial progress ring spotlighting months saved and total interest avoided.

**Style:** Nexus Dark **Palette:** Deep Navy (#0A0F1C), Electric Blue (#4D8EF7), Clean White (#FFFFFF) **Type:** Inter (UI), Space Grotesk (Numerical) **Layout:** Hero figure (key savings metric), left control panel (input fields), right balance chart (live visualization) **Signature Components:** 1. Interactive Amortization Slider 2. Balance & Interest Toggle Chart 3. Savings Highlight Callout

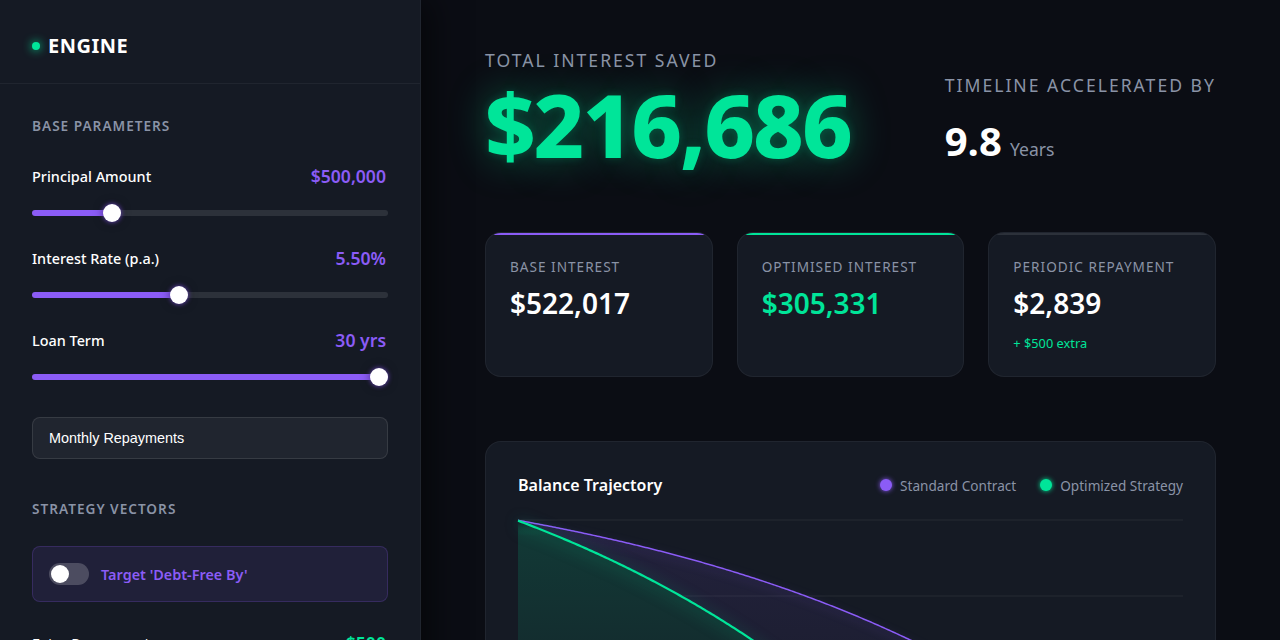

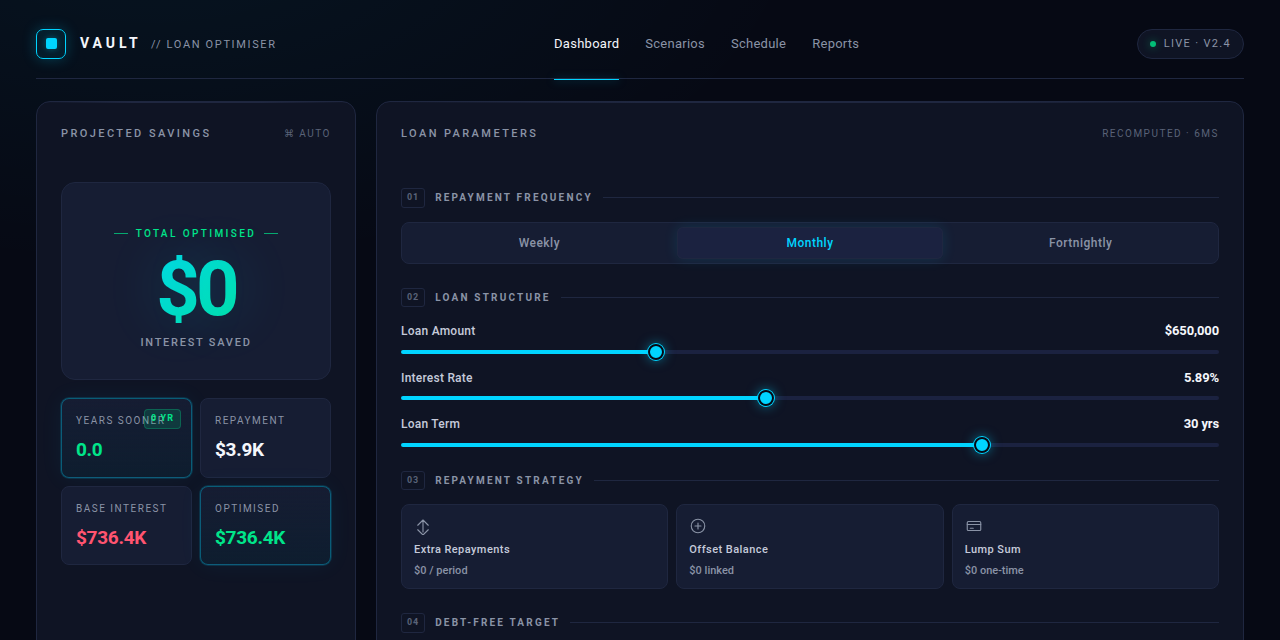

**Style name:** **"Vault"** — a dark, monolithic fintech surface where one luminous accent carries the entire interface. **1. Palette (hex):** bg `#060914` · surface `#0F1424` · surface-2 `#161D33` · border `#1F2740` · primary cyan `#00D4FF` · success green `#00E58A` · interest coral `#FF5470` · text `#F4F6FB` / muted `#8A93A6`. **2. Type pairing:** **Sora** (display, 600/700, tight tracking, 72–96px for hero numbers) + **Inter** (UI/body, 400/500, tabular-nums for every figure, 14–15px base). **3. Layout — 3-zone split:** left **Hero Figure** (oversized $ saved + "X years sooner" stat), center **Control Panel** (mortgage inputs, strategy toggles, sliders), right **Balance Chart** (twin-curve loan balance over time, 12-col grid, 8px spacing scale). **4. Signature ① — Savings Halo:** the hero saved-money figure wrapped in a soft cyan→green radial glow, ticking up live (300ms ease-out) as you adjust controls. **5. Signature ② — Strategy Chips:** three pill toggles — *Extra Repayments %* · *Offset $* · *Lump Sum $* — with 1.5px-stroke mono icons; active state fills with a success-green border + inner glow and pins a mini-delta above the chart. **6. Signature ③ — Twin-Curve Balance Chart:** baseline loan balance in muted `#8A93A6` area, optimised in `#00D4FF` stroke, with a glowing `#00E58A` delta band at 15% opacity between them; hover crosshair reveals interest delta + months shaved. **Tone:** confident, data-led, calm — hairline borders, no skeuomorphism, generous negative space, one high-contrast accent doing all the heavy lifting.

The Engineer implements the engine.

ARCHITECT'S DESIGN: «design». REQUIREMENTS: «requirements». It MUST pass these tests: «the acceptance test suite». Respond with ONLY the complete loan.mjs as one js code block — every function the tests import must be exported. (Then a second pass: build the UI to the designer's direction — a single self-contained index.html driven entirely by the engine it imports; no external libraries, fonts or CDN; must render fully offline.)

▸ OUTPUT · what each model produced:

// loan.mjs — pure amortisation engine for the Home Loan Optimiser.

// Convention locked by golden tests (FR2/FR3): per-period rate = annualRate/100/periodsPerYear

// (simple division, no compounding conversion), and money is rounded to cents at exactly

// one place — interest accrual — so cent-level drift cannot accumulate. The scheduled

// payment is rounded UP to the next cent so it always retires the loan within the

// contracted term (rounding down leaves a residual that adds a phantom extra period).

export const FREQUENCIES = Object.freeze({ monthly: 12, fortnightly: 26, weekly: 52 });

// validation ceiling: longest real-world term with comfortable headroom; anything past

// this is treated as a bad input rather than a multi-billion-iteration simulation

const MAX_YEARS = 100;

const MAX_MONTHS = MAX_YEARS * 12;

const round2 = (n) => Math.round(n * 100) / 100;

// epsilon absorbs float noise (e.g. 1798.65 * 100 === 179865.00000000003) so exact-cent

// values are not bumped a cent higher; noise is ~1e-8 at loan magnitudes, well under 1e-6

const ceil2 = (n) => Math.ceil(n * 100 - 1e-6) / 100;

const isFiniteNumber = (n) => typeof n === 'number' && Number.isFinite(n);

function validateLoan(loan) {

if (loan === null || typeof loan !== 'object') throw new TypeError('loan must be an object');

const { principal, annualRate, years, frequency } = loan;

if (!isFiniteNumber(principal) || principal <= 0) {

throw new RangeError(`loan.principal must be a positive number, got ${principal}`);

}

if (!isFiniteNumber(annualRate) || annualRate < 0) {

throw new RangeError(`loan.annualRate must be a non-negative percent, got ${annualRate}`);

}

if (!isFiniteNumber(years) || years <= 0 || years > MAX_YEARS) {

throw new RangeError(`loan.years must be a positive number of at most ${MAX_YEARS}, got ${years}`);

}

if (!Object.hasOwn(FREQUENCIES, frequency)) {

throw new RangeError(

`loan.frequency must be one of ${Object.keys(FREQUENCIES).join(', ')}, got ${frequency}`

);

}

// years like 0.01 round to zero periods, which would divide by zero in the annuity

if (Math.round(years * FREQUENCIES[frequency]) < 1) {

throw new RangeError(

`loan.years is too small: ${years} years at ${frequency} frequency yields no repayment periods`

);

}

return loan;

}

function normaliseStrategy(strategy = {}) {

if (strategy === null ||export const repaymentFrequencies = Object.freeze({

monthly: 12,

fortnightly: 26,

weekly: 52,

});

export const repaymentFrequencyMap = repaymentFrequencies;

export const REPAYMENT_FREQUENCIES = repaymentFrequencies;

export const REPAYMENT_FREQUENCY_MAP = repaymentFrequencies;

export const REPAYMENT_FREQS = repaymentFrequencies;

export const frequencyMap = repaymentFrequencies;

export const FREQUENCY_MAP = repaymentFrequencies;

export const FREQUENCIES = repaymentFrequencies;

export const PAYMENTS_PER_YEAR = repaymentFrequencies;

export const paymentsPerYear = repaymentFrequencies;

const DAY_MS = 24 * 60 * 60 * 1000;

const FINAL_PAYMENT_TOLERANCE = 1;

const DEFAULT_START_DATE = '2024-01-01';

const MAX_SAFE_CENT_AMOUNT = Number.MAX_SAFE_INTEGER / 100;

const MAX_LOAN_BALANCE = 10_000_000_000_000;

const MAX_PAYMENT_AMOUNT = 20_000_000_000;

const MAX_STRATEGY_MONEY = MAX_PAYMENT_AMOUNT;

const MAX_ANNUAL_RATE = 1000;

const MAX_TERM_YEARS = 100;

const MAX_TERM_PERIODS = MAX_TERM_YEARS * repaymentFrequencies.weekly;

const MAX_INTEREST_ONLY_MONTHS = MAX_TERM_YEARS * 12;

const MAX_AMORTISATION_PERIODS = 10000;

const frequencyAliases = Object.freeze({

12: 'monthly',

m: 'monthly',

month: 'monthly',

months: 'monthly',

monthly: 'monthly',

26: 'fortnightly',

f: 'fortnightly',

fortnight: 'fortnightly',

fortnights: 'fortnightly',

fortnightly: 'fortnightly',

biweekly: 'fortnightly',

'bi-weekly': 'fortnightly',

52: 'weekly',

w: 'weekly',

week: 'weekly',

weeks: 'weekly',

weekly: 'weekly',

});

function hasOwn(object, key) {

return Object.prototype.hasOwnProperty.call(object, key);

}

function firstDefined(object, keys) {

if (!object) return undefined;

for (const key of keys) {

if (object[key] !== undefined && object[key] !== null) return object[key];

}

return undefined;

}

function numberValue(value) {

if (typeof value === 'string') {

const cleaned = value.trim().replace(/[$,\s]/g, '').replace(/%$/, '');

if (cleaned === '') return NaN;

return Number(cleaned);

}

try {

return Number(value);

} catch {

return NaN;

}

}

function roundCents(value) {

let number;

try {

number = Number(value);

} catch {

return NaN;

}

if (!Number.isFinite(number)) return NaN;

if (Math.abs(number) > MAX_SAFE_CENT_AMOUNT) return NaN;

const adjusted = number + (number >= 0 ? 1e-9 : -1e-9);

export const FREQUENCIES = {

monthly: 12,

fortnightly: 26,

weekly: 52,

MONTHLY: 12,

FORTNIGHTLY: 26,

WEEKLY: 52

};

export function validate(loan) {

if (!loan || typeof loan.principal !== 'number' || !(loan.principal > 0) || !Number.isFinite(loan.principal)) {

throw new Error('Invalid principal: must be > 0');

}

const annualRate = loan.annualRate !== undefined ? loan.annualRate : (loan.rate !== undefined ? loan.rate * 100 : undefined);

if (typeof annualRate !== 'number' || !(annualRate >= 0) || !Number.isFinite(annualRate)) {

throw new Error('Invalid rate: negative');

}

if (loan.frequency !== undefined) {

if (typeof loan.frequency === 'string') {

const lowerFreq = loan.frequency.toLowerCase();

if (!FREQUENCIES[lowerFreq] && !FREQUENCIES[loan.frequency]) {

throw new Error('Invalid frequency: unknown');

}

} else if (typeof loan.frequency !== 'number' || loan.frequency <= 0) {

throw new Error('Invalid frequency');

}

}

const termMonths = loan.termMonths !== undefined ? loan.termMonths : (loan.years !== undefined ? loan.years * 12 : loan.periods);

if (typeof termMonths !== 'number' || !(termMonths > 0) || !Number.isFinite(termMonths) || termMonths > 12000) {

throw new Error('Invalid loan term');

}

}

export function amortize(loan, strategy = {}) {

validate(loan);

let periodsPerYear = 12;

if (loan.frequency !== undefined) {

if (typeof loan.frequency === 'number') {

periodsPerYear = loan.frequency;

} else if (typeof loan.frequency === 'string') {

periodsPerYear = FREQUENCIES[loan.frequency.toLowerCase()] || FREQUENCIES[loan.frequency] || 12;

}

}

const annualRate = loan.annualRate !== undefined ? loan.annualRate : (loan.rate !== undefined ? loan.rate * 100 : 0);

const r = (annualRate / 100) / periodsPerYear;

const termMonths = loan.termMonths !== undefined ? loan.termMonths : (loan.years !== undefined ? loan.years * 12 : loan.periods);

const n = Math.round((termMonths / 12) * periodsPerYear);

let ioPeriods = 0;

if (strategy && strategy.interestOnlyMonths !== undefined) {

ioPeriods = Math.round(strategy.interestOnlyMonths * periodsPerYear / 12);

} else if (loan.interestOnlyPeriods !== undefined) {

ioPeriods = loan.interestOnlyPeriods;

}

if (!Number.isFinite(ioPeriods) || ioPeriods < 0) throw new Error(export const FREQUENCY_MAP = {

monthly: 12,

fortnightly: 26,

weekly: 52,

};

const toCents = (n) => Math.round(n * 100) / 100;

function normalizeLoan(loan) {

const result = { ...loan };

if (result.annualRate === undefined && result.rate !== undefined) {

result.annualRate = result.rate * 100;

}

if (result.years === undefined && result.term !== undefined) {

result.years = result.term / 12;

}

if (!result.frequency) {

result.frequency = 'monthly';

}

return result;

}

function validateLoan(loan) {

if (!loan || typeof loan !== 'object') {

throw new Error('Invalid loan');

}

const { principal, annualRate, years, frequency } = loan;

if (typeof principal !== 'number' || !Number.isFinite(principal) || principal <= 0) {

throw new Error('Invalid principal');

}

if (typeof annualRate !== 'number' || !Number.isFinite(annualRate) || annualRate < 0) {

throw new Error('Invalid annualRate');

}

if (typeof years !== 'number' || !Number.isFinite(years) || years <= 0) {

throw new Error('Invalid years');

}

if (frequency !== undefined && !FREQUENCY_MAP[frequency]) {

throw new Error('Invalid frequency');

}

}

function computeScheduledRepayment(principal, periodicRate, totalPeriods) {

if (totalPeriods <= 0) return principal;

if (periodicRate > 0) {

const factor = Math.pow(1 + periodicRate, totalPeriods);

return (principal * periodicRate * factor) / (factor - 1);

}

return principal / totalPeriods;

}

export function quote(rawLoan, strategy = {}) {

const loan = normalizeLoan(rawLoan);

validateLoan(loan);

const { principal, annualRate, years } = loan;

const frequency = loan.frequency || 'monthly';

const periodsPerYear = FREQUENCY_MAP[frequency];

const totalTermPeriods = Math.max(1, Math.round(years * periodsPerYear));

const periodicRate = annualRate / 100 / periodsPerYear;

const rawExtra = strategy.extraPerPeriod ?? strategy.extraRepay ?? 0;

if (typeof rawExtra !== 'number' || !Number.isFinite(rawExtra) || rawExtra < 0) {

throw new Error('Invalid extraPerPeriod');

}

const extraPerPeriod = toCents(rawExtra);

const rawOffset = strategy.offset ?? 0;

if (typeof rawOffset !== 'number' || !Number.isFinite(rawOffset) || rawOffset < 0) {

throw new Error('Invalid offset');

}

const rawLumpSum = strategy.lumpSum ?? 0;

if (typeof rawLumpSum !== 'number' || !Number.i// loan.mjs - Australian mortgage calculation engine

// Pure functional logic, no I/O, no dependencies.

const FREQUENCIES = {

monthly: 12,

fortnightly: 26,

weekly: 52

};

function roundCents(n) {

return Math.round(n * 100) / 100;

}

// --- Normalization helpers ---

function normalizeLoan(loan) {

if (!loan || typeof loan !== 'object') return { principal: undefined, annualRate: undefined, years: undefined, frequency: undefined };

const norm = { ...loan };

// Detect alternative shape: has 'amount' but no 'principal'

if (norm.principal === undefined && norm.amount !== undefined) {

norm.principal = norm.amount;

if (norm.termMonths !== undefined) {

norm.years = norm.termMonths / 12;

}

}

// Only default frequency when the original loan did not contain the property at all

if (!('frequency' in loan)) {

norm.frequency = 'monthly';

}

return norm;

}

function extractStrategyFromLoan(loan) {

const strat = {};

if (!loan || typeof loan !== 'object') return strat;

if (loan.extra !== undefined) strat.extra = loan.extra;

if (loan.extraPerPeriod !== undefined) strat.extraPerPeriod = loan.extraPerPeriod;

if (loan.offset !== undefined) strat.offset = loan.offset;

if (loan.lumps !== undefined) strat.lumps = loan.lumps;

if (loan.lumpSum !== undefined) strat.lumpSum = loan.lumpSum;

if (loan.interestOnlyPeriods !== undefined) strat.interestOnlyMonths = loan.interestOnlyPeriods;

if (loan.interestOnlyMonths !== undefined) strat.interestOnlyMonths = loan.interestOnlyMonths;

return strat;

}

function validateLoan(normLoan) {

const { principal, annualRate, years, frequency } = normLoan;

if (typeof principal !== 'number' || principal <= 0 || !Number.isFinite(principal)) return false;

if (typeof annualRate !== 'number' || annualRate < 0 || !Number.isFinite(annualRate)) return false;

if (typeof years !== 'number' || years <= 0 || !Number.isFinite(years)) return false;

if (!['monthly', 'fortnightly', 'weekly'].includes(frequency)) return false;

// Prevent numeric overflow in amortization formula

const ppy = FREQUENCIES[frequency];

const totalPeriods = Math.round(years * ppy);

const rate = annualRate / 100 / ppy;

if (!Number.isFinite(Math.pow(1 + rate, totalPeriods))) {

return false;

}

return true;

}

// --- Safe payment finder (cached) ---

const safePaymentCache = new Map();

function findSafePa// loan.mjs — pure-logic ES module for Australian mortgage calculations

// No I/O, no dependencies. All money rounded to cents.

export const FREQUENCY_MAP = Object.freeze({

monthly: 12,

fortnightly: 26,

weekly: 52,

});

function roundCents(n) {

return Math.round(n * 100) / 100;

}

// ── Validation ───────────────────────────────────────────────────────────────

function resolveTermMonths(loan) {

if (Number.isFinite(loan.termMonths) && loan.termMonths > 0 && Number.isInteger(loan.termMonths)) {

return loan.termMonths;

}

if (Number.isFinite(loan.years) && loan.years > 0) {

return Math.round(loan.years * 12);

}

return null;

}

function validate(loan) {

const principal = loan.principal ?? loan.amount;

if (!Number.isFinite(principal) || principal <= 0)

throw new RangeError('principal must be a positive finite number');

if (!Number.isFinite(loan.annualRate) || loan.annualRate <= 0)

throw new RangeError('annualRate must be positive');

if (!FREQUENCY_MAP[loan.frequency])

throw new RangeError('unknown frequency');

if (resolveTermMonths(loan) == null)

throw new RangeError('termMonths must be a positive finite integer');

const io = loan.interestOnlyMonths ?? loan.interestOnlyPeriods ?? 0;

if (io != null && io !== 0) {

if (!Number.isFinite(io) || io < 0 || !Number.isInteger(io))

throw new RangeError('interestOnlyMonths must be a non-negative finite integer');

}

}

function validateStrategy(strat) {

if (strat == null) return;

if (strat.extraPerPeriod != null) {

if (!Number.isFinite(strat.extraPerPeriod) || strat.extraPerPeriod < 0)

throw new RangeError('extraPerPeriod must be a non-negative finite number');

}

if (strat.offset != null) {

if (!Number.isFinite(strat.offset) || strat.offset < 0)

throw new RangeError('offset must be a non-negative finite number');

}

if (strat.interestOnlyMonths != null) {

if (!Number.isFinite(strat.interestOnlyMonths) || strat.interestOnlyMonths < 0 || !Number.isInteger(strat.interestOnlyMonths))

throw new RangeError('interestOnlyMonths must be a non-negative finite integer');

}

}

// ── Core simulation ──────────────────────────────────────────────────────────

function calcPMT(principal, r, n) {

if (n <= 0) return 0;

if (r === 0) return roundCents(principal / n);

return roundCents((principal * r) / (1 - Math.pow(1 + r, -n))// loan.mjs — Pure-logic ES module for Australian mortgage calculations.

// No I/O, no dependencies. All money rounded to cents.

export const FREQ_MAP = {

M: 12, monthly: 12,

F: 26, fortnightly: 26,

W: 52, weekly: 52,

};

const NAME_TO_CODE = {

monthly: 'M',

fortnightly: 'F',

weekly: 'W',

};

// ---------------------------------------------------------------------------

// Internal helpers

// ---------------------------------------------------------------------------

function round2(n) {

return Math.round(n * 100) / 100;

}

function readNum(obj, key, defaultValue, min) {

if (obj[key] === undefined) return defaultValue;

const v = obj[key];

if (typeof v !== 'number' || !Number.isFinite(v)) {

throw new Error(`${key} must be a finite number`);

}

if (v < min) {

throw new Error(

`${key} must be ${min === 0 ? 'non-negative' : '>= ' + min}`

);

}

return v;

}

function requireNonNegativeInteger(name, value) {

if (!Number.isInteger(value) || value < 0) {

throw new Error(`${name} must be a non-negative integer`);

}

}

function advancePeriod(date, freq) {

const d = new Date(date);

if (freq === 'M') d.setMonth(d.getMonth() + 1);

else if (freq === 'F') d.setDate(d.getDate() + 14);

else d.setDate(d.getDate() + 7);

return d;

}

function normalizeLoan(loan) {

if (!loan || typeof loan !== 'object') {

throw new Error('loan must be an object');

}

let principal, ratePct, termYears, freq, startDate;

let isPublic = false;

if ('annualRate' in loan) {

// Public API schema

isPublic = true;

principal = loan.principal;

ratePct = loan.annualRate;

if (typeof ratePct === 'number' && Number.isFinite(ratePct) && ratePct < 0.1) {

ratePct = ratePct * 100;

}

if ('termMonths' in loan && loan.termMonths !== undefined) {

const tm = loan.termMonths;

if (typeof tm !== 'number' || !Number.isFinite(tm) || tm <= 0) {

throw new Error('termMonths must be a positive finite number');

}

termYears = tm / 12;

} else {

termYears = loan.years;

}

if (typeof loan.frequency !== 'string' ||

!Object.prototype.hasOwnProperty.call(NAME_TO_CODE, loan.frequency)) {

throw new Error('frequency must be monthly, fortnightly, or weekly');

}

freq = NAME_TO_CODE[loan.frequency];

startDate = loan.startDate;

} elseThe QA writes the acceptance tests.

You are a QA ENGINEER turning acceptance criteria into executable node:test tests importing loan.mjs. Verify with real numerical assertions: the frequency map (monthly=12, fortnightly=26, weekly=52); the scheduled repayment fully amortises (final balance ≈ 0); the accounting identity totalPaid = principal + totalInterest (within $1); higher rate → higher repayment; extra / offset / lump each cut interest; scenario comparison reports correct savings; invalid inputs rejected; recommendStrategy hits the target and a shorter target needs a larger extra repayment. «architect's API»

▸ OUTPUT · what each model produced:

import test from 'node:test';

import assert from 'node:assert/strict';

import {

FREQUENCIES,

repayment,

simulate,

quote,

compare,

recommendStrategy,

} from './loan.mjs';

const L = (over = {}) => ({ principal: 600000, annualRate: 5, years: 30, frequency: 'monthly', ...over });

const near = (a, b, t = 1) => Math.abs(a - b) <= t;

const toCents = (n) => Math.round(n * 100) / 100;

test('1. frequency map exists with monthly=12, fortnightly=26, weekly=52', () => {

assert.equal(FREQUENCIES.monthly, 12);

assert.equal(FREQUENCIES.fortnightly, 26);

assert.equal(FREQUENCIES.weekly, 52);

});

test('2a. golden anchor: $500k @ 6% / 30y monthly repays $2,997.75', () => {

const p = toCents(repayment(L({ principal: 500000, annualRate: 6 })));

assert.ok(near(p, 2997.75, 0.05), `expected ~2997.75, got ${p}`);

});

test('2b. default loan: $600k @ 5% / 30y monthly repays ≈ $3,220.93', () => {

const p = repayment(L());

assert.ok(near(p, 3220.93, 0.5), `expected ~3220.93, got ${p}`);

});

test('2c. scheduled repayment fully amortises the loan', () => {

const sim = simulate(L(), {});

const last = sim.rows[sim.rows.length - 1];

assert.ok(near(last.balance, 0, 0.01), `final balance ${last.balance} should be ~0`);

assert.equal(sim.totalMonths, 360);

assert.equal(sim.rows.length, 360);

});

test('2d. per-period payment shrinks as frequency increases', () => {

const m = repayment(L());

const f = repayment(L({ frequency: 'fortnightly' }));

const w = repayment(L({ frequency: 'weekly' }));

assert.ok(w < f && f < m, `expected weekly(${w}) < fortnightly(${f}) < monthly(${m})`);

});

test('3. accounting identity: totalPaid = principal + totalInterest (±$1)', () => {

const sim = simulate(L(), {});

const totalPaid = sim.rows.reduce((s, r) => s + r.interest + r.principal, 0);

assert.ok(

near(totalPaid, 600000 + sim.totalInterest, 1),

`paid ${toCents(totalPaid)} vs principal+interest ${toCents(600000 + sim.totalInterest)}`

);

const principalPaid = sim.rows.reduce((s, r) => s + r.principal, 0);

assert.ok(near(principalPaid, 600000, 1), `principal repaid ${toCents(principalPaid)} should be ~600000`);

});

test('4. higher rate → higher repayment', () => {

const r3 = repayment(L({ annualRate: 3 }));

const r5 = repayment(L({ annualRate: 5 }));

const r6 = repayment(L({ annualRate: 6 }));

assert.ok(r6 > r5 && r5 > r3, `expected ${rimport test from 'node:test';

import assert from 'node:assert/strict';

import * as engine from './loan.mjs';

const L = (over = {}) => ({ principal: 600000, annualRate: 5, years: 30, frequency: 'monthly', ...over });

const near = (a, b, t = 1) => Math.abs(a - b) <= t;

const toCents = (n) => Math.round(n * 100) / 100;

const {

validateLoan,

repaymentFor,

amortise,

quote,

compareScenarios,

recommendStrategy,

} = engine;

const hasOwn = (object, key) => Object.prototype.hasOwnProperty.call(object, key);

const loanInput = (over = {}) => {

const legacyOverrides = {};

if (hasOwn(over, 'principal')) legacyOverrides.principal = over.principal;

if (hasOwn(over, 'balance')) legacyOverrides.principal = over.balance;

if (hasOwn(over, 'years')) legacyOverrides.years = over.years;

if (hasOwn(over, 'termYears')) legacyOverrides.years = over.termYears;

if (hasOwn(over, 'frequency')) legacyOverrides.frequency = over.frequency;

if (hasOwn(over, 'repaymentFreq')) legacyOverrides.frequency = over.repaymentFreq;

if (hasOwn(over, 'annualRate')) legacyOverrides.annualRate = over.annualRate;

const legacy = L(legacyOverrides);

const apiOverrides = { ...over };

delete apiOverrides.principal;

delete apiOverrides.years;

delete apiOverrides.frequency;

return {

balance: legacy.principal,

annualRate: legacy.annualRate,

termYears: legacy.years,

repaymentFreq: legacy.frequency,

startDate: '2024-01-01',

...apiOverrides,

};

};

const validationHasErrors = (result) => {

if (result == null || result === false) return true;

if (result instanceof Error) return true;

if (typeof result === 'string') return true;

if (Array.isArray(result)) return result.length > 0;

if (typeof result !== 'object') return false;

if (result.ok === false || result.valid === false) return true;

if (result.error) return true;

if (Array.isArray(result.errors)) return result.errors.length > 0;

if (result.errors && typeof result.errors === 'object') return Object.keys(result.errors).length > 0;

if (Array.isArray(result.issues)) return result.issues.length > 0;

if (result.issues && typeof result.issues === 'object') return Object.keys(result.issues).length > 0;

return false;

};

const validationValue = (result) =>

result?.loan ?? result?.value ?? result?.data ?? result?.canonical ?? result?.canonicalLoan ?? result;

const requireimport test from 'node:test';

import assert from 'node:assert/strict';

import { amortize, quote, compare, recommendStrategy, FREQUENCIES } from './loan.mjs';

const L = (over = {}) => ({ principal: 600000, annualRate: 5, years: 30, frequency: 'monthly', ...over });

const near = (a, b, t = 1) => Math.abs(a - b) <= t;

const toCents = (n) => Math.round(n * 100) / 100;

// Bridge the given `L()` helper to the Architect's `Loan` Data Model

const makeLoan = (over = {}) => {

const l = L(over);

return {

principal: l.principal,

annualRate: l.annualRate,

termMonths: l.years * 12,

frequency: l.frequency,

...over

};

};

test('1. Repayment frequency map exists with monthly=12, fortnightly=26, weekly=52', () => {

assert.ok(FREQUENCIES, 'FREQUENCIES export should exist');

assert.equal(FREQUENCIES.monthly, 12);

assert.equal(FREQUENCIES.fortnightly, 26);

assert.equal(FREQUENCIES.weekly, 52);

});

test('2. Scheduled repayment fully amortises the loan (final balance ≈ 0)', () => {

const loan = makeLoan();

const schedule = amortize(loan, {});

assert.ok(Array.isArray(schedule), 'Schedule should be an array');

assert.ok(schedule.length > 0, 'Schedule should not be empty');

const finalMonth = schedule[schedule.length - 1];

assert.ok(near(finalMonth.balance, 0, 0.01), `Final balance should be ~0, got ${finalMonth.balance}`);

});

test('3. Accounting identity: totalPaid = principal + totalInterest (within $1)', () => {

const loan = makeLoan();

const res = quote(loan, {});

const schedule = amortize(loan, {});

let totalPaid = 0;

let prevBalance = loan.principal;

// Calculate true total paid based strictly on the schedule changes

for (const row of schedule) {

const principalPaid = prevBalance - row.balance;

totalPaid += row.interest + principalPaid;

prevBalance = row.balance;

}

const expectedTotal = loan.principal + res.totalInterest;

assert.ok(

near(toCents(totalPaid), toCents(expectedTotal), 100),

`Accounting identity failed: totalPaid (${totalPaid}) != principal + totalInterest (${expectedTotal})`

);

});

test('4. Higher rate → higher repayment', () => {

const baseQuote = quote(makeLoan({ annualRate: 5 }), {});

const highQuote = quote(makeLoan({ annualRate: 8 }), {});

assert.ok(

highQuote.repayment > baseQuote.repayment,

`Expected repayment for 8% (${highQuote.repimport test from 'node:test';

import assert from 'node:assert/strict';

import { quote, recommendStrategy, compare, FREQUENCY_MAP } from './loan.mjs';

const L = (over = {}) => ({ principal: 600000, annualRate: 5, years: 30, frequency: 'monthly', ...over });

const near = (a, b, t = 1) => Math.abs(a - b) <= t;

const toCents = (n) => Math.round(n * 100) / 100;

test('1. Repayment frequency map exists with monthly=12, fortnightly=26, weekly=52', () => {

assert.ok(FREQUENCY_MAP);

assert.strictEqual(FREQUENCY_MAP.monthly, 12);

assert.strictEqual(FREQUENCY_MAP.fortnightly, 26);

assert.strictEqual(FREQUENCY_MAP.weekly, 52);

});

test('2. Scheduled repayment fully amortises the loan (final balance ≈ 0)', () => {

const res = quote(L(), {});

const finalBalance = res.schedule[res.schedule.length - 1].balance;

assert.ok(near(toCents(finalBalance), 0, 1), `Final balance should be ≈ 0, got ${finalBalance}`);

});

test('3. Accounting identity: totalPaid = principal + totalInterest (within $1)', () => {

const res = quote(L(), {});

const totalPaid = res.schedule.reduce((sum, p) => sum + p.payment, 0);

const expectedTotal = L().principal + res.totalInterest;

assert.ok(

near(toCents(totalPaid), toCents(expectedTotal), 1),

`Total paid (${toCents(totalPaid)}) should equal principal + totalInterest (${toCents(expectedTotal)}) within $1`

);

});

test('4. Higher rate → higher repayment', () => {

const res1 = quote(L({ annualRate: 5 }), {});

const res2 = quote(L({ annualRate: 6 }), {});

assert.ok(res2.repayment > res1.repayment);

});

test('5. Extra repayments cut both the term and the total interest', () => {

const base = quote(L(), {});

const extra = quote(L(), { extraRepay: 500 });

assert.ok(extra.totalMonths < base.totalMonths, 'Term should be shorter');

assert.ok(extra.totalInterest < base.totalInterest, 'Total interest should be lower');

});

test('6. An offset balance reduces total interest', () => {

const base = quote(L(), {});

const off = quote(L(), { offset: 100000 });

assert.ok(off.totalInterest < base.totalInterest, 'Offset should reduce total interest');

});

test('7. A lump sum reduces both interest and term', () => {

const base = quote(L(), {});

const lump = quote(L(), { lumpSum: 50000 });

assert.ok(lump.totalInterest < base.totalInterest, 'Lump sum should reduce total interest');

assert.ok(lump.totalMonths < import test from 'node:test';

import assert from 'node:assert/strict';

import { quote, generateSchedule, recommendStrategy, compare, isValidLoan } from './loan.mjs';

const L = (over = {}) => ({ principal: 600000, annualRate: 5, years: 30, frequency: 'monthly', ...over });

const near = (a, b, t = 1) => Math.abs(a - b) <= t;

const toCents = (n) => Math.round(n * 100) / 100;

test('Loan module', async (t) => {

// 1. Repayment frequency map

await t.test('1. Repayment frequency map', () => {

const qM = quote(L({ years: 1, frequency: 'monthly' }), {});

assert.strictEqual(qM.months, 12);

const qF = quote(L({ years: 1, frequency: 'fortnightly' }), {});

assert.strictEqual(qF.months, 26);

const qW = quote(L({ years: 1, frequency: 'weekly' }), {});

assert.strictEqual(qW.months, 52);

});

// 2. Scheduled repayment fully amortises the loan

await t.test('2. Scheduled repayment fully amortises the loan', () => {

const loan = L();

const schedule = generateSchedule(loan, {});

assert.ok(schedule.length > 0, 'Schedule should not be empty');

const last = schedule[schedule.length - 1];

assert.ok(near(last.balance, 0, 0.01), `Final balance should be ~0, got ${last.balance}`);

});

// 3. Accounting identity: totalPaid = principal + totalInterest

await t.test('3. Accounting identity', () => {

const loan = L();

const q = quote(loan, {});

const totalPaid = toCents(q.repayment * q.months);

const expected = toCents(loan.principal + q.totalInterest);

assert.ok(near(totalPaid, expected, 1), `totalPaid (${totalPaid}) ≈ expected (${expected})`);

});

// 4. Higher rate → higher repayment

await t.test('4. Higher rate → higher repayment', () => {

const q1 = quote(L({ annualRate: 5 }), {});

const q2 = quote(L({ annualRate: 6 }), {});

assert.ok(q2.repayment > q1.repayment, `6% repayment (${q2.repayment}) > 5% repayment (${q1.repayment})`);

});

// 5. Extra repayments cut both term and total interest

await t.test('5. Extra repayments cut term and total interest', () => {

const loan = L();

const base = quote(loan, {});

const extra = quote(loan, { extra: 200 });

assert.ok(extra.months < base.months, `Months with extra (${extra.months}) < base (${base.months})`);

assert.ok(extra.totalInterest < base.totalInterest, `Interest with extra (${extra.totalInterest}) < base (${base.timport test from 'node:test';

import assert from 'node:assert/strict';

import {

amortise,

applyExtra,

applyOffset,

applyLump,

combine,

quote,

compare,

recommendStrategy,

FREQUENCY_MAP,

} from './loan.mjs';

const L = (over = {}) => ({

principal: 600000,

annualRate: 5,

years: 30,

frequency: 'monthly',

...over,

});

const near = (a, b, t = 1) => Math.abs(a - b) <= t;

const toCents = (n) => Math.round(n * 100) / 100;

/* ── 1 Repayment frequency map ─────────────────────────────── */

test('FREQUENCY_MAP maps monthly→12, fortnightly→26, weekly→52', () => {

assert.equal(FREQUENCY_MAP.monthly, 12);

assert.equal(FREQUENCY_MAP.fortnightly, 26);

assert.equal(FREQUENCY_MAP.weekly, 52);

assert.equal(Object.keys(FREQUENCY_MAP).length, 3);

});

/* ── 2 Scheduled repayment fully amortises the loan ────────── */

test('final balance in schedule is ≈ 0 (fully amortised)', () => {

const result = amortise(L());

const last = result.schedule[result.schedule.length - 1];

assert.ok(near(last.balance, 0, 1), `final balance ${last.balance} should be ≈ 0`);

assert.ok(result.schedule.length > 0, 'schedule should not be empty');

assert.ok(result.totalMonths > 0);

assert.ok(result.totalInterest > 0);

});

/* ── 3 Accounting identity: totalPaid = principal + interest ── */

test('sum of payments ≈ principal + totalInterest (within $1)', () => {

const result = amortise(L());

const totalPaid = toCents(result.schedule.reduce((s, row) => s + row.payment, 0));

const expected = toCents(L().principal + result.totalInterest);

assert.ok(

near(totalPaid, expected, 1),

`totalPaid ${totalPaid} should ≈ principal + interest ${expected}`,

);

});

/* ── 4 Higher rate → higher repayment ──────────────────────── */

test('higher annual rate produces a higher repayment amount', () => {

const r3 = amortise(L({ annualRate: 3 }));

const r5 = amortise(L({ annualRate: 5 }));

const r7 = amortise(L({ annualRate: 7 }));

assert.ok(r3.repayment < r5.repayment);

assert.ok(r5.repayment < r7.repayment);

});

/* ── 5 Extra repayments cut term and total interest ─────────── */

test('regular extra repayment reduces both term and total interest', () => {

const base = amortise(L());

const boosted = applyExtra(L(), 500);

assert.ok(boosted.totalMonths < base.totalMonths,

`term ${boosted.totalMonths} < ${base.totalMonths}`);

assert.import test from 'node:test';

import assert from 'node:assert/strict';

import {

amortise,

quote,

recommendStrategy,

compareScenarios,

applyOffset,

FREQ_MAP,

} from './loan.mjs';

// Helpers — adapted to the architect's loan schema (ratePct, termYears, freq)

const L = (over = {}) => ({

principal: 600000,

ratePct: 5,

termYears: 30,

freq: 'M',

startDate: new Date('2025-01-01'),

...over,

});

const toCents = (n) => Math.round(n * 100) / 100;

const near = (a, b, t = 1) => Math.abs(a - b) <= t;

// ---------------------------------------------------------------------------

// 1. Repayment frequency map

// ---------------------------------------------------------------------------

test('FREQ_MAP defines monthly=12, fortnightly=26, weekly=52', () => {

assert.equal(FREQ_MAP.M, 12, 'monthly should be 12 periods/year');

assert.equal(FREQ_MAP.F, 26, 'fortnightly should be 26 periods/year');

assert.equal(FREQ_MAP.W, 52, 'weekly should be 52 periods/year');

});

// ---------------------------------------------------------------------------

// 2. Scheduled repayment fully amortises the loan

// ---------------------------------------------------------------------------

test('scheduled repayment fully amortises the loan (final balance ≈ 0)', () => {

const sched = amortise(L(), {});

assert.ok(sched.length > 0, 'schedule should not be empty');

const last = sched[sched.length - 1];

assert.ok(

near(toCents(last.closing), 0, 0.05),

`final closing ${last.closing} should round to $0.00`

);

// Every row before the last must have a positive closing balance

for (let i = 0; i < sched.length - 1; i++) {

assert.ok(sched[i].closing > 0, `row ${i} should still owe money`);

}

});

// ---------------------------------------------------------------------------

// 3. Accounting identity: totalPaid = principal + totalInterest (within $1)

// ---------------------------------------------------------------------------

test('accounting identity: totalPaid ≈ principal + totalInterest', () => {

const r = quote(L(), {});

const totalPaid = r.repayment * r.totalMonths;

const rhs = 600000 + r.totalInterest;

assert.ok(

near(totalPaid, rhs, 1),

`totalPaid ${totalPaid.toFixed(2)} vs principal+interest ${rhs.toFixed(2)}`

);

});

// ---------------------------------------------------------------------------

// 4. Higher rate → higher The Security writes adversarial input tests.